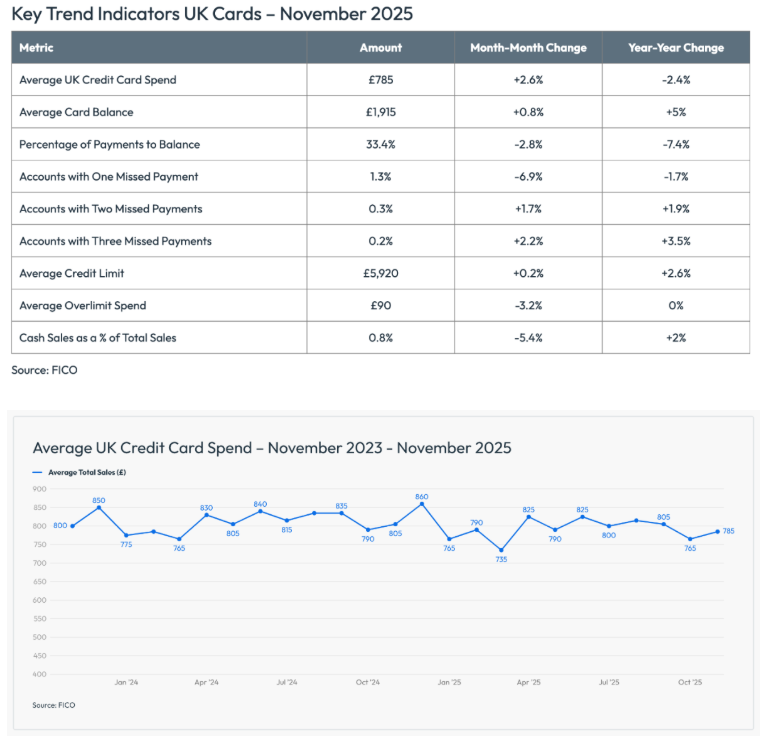

Credit card spending rose by 2.6% between October and November

Analysis of credit card data for November 2025 by global analytics software leader FICO has found that spending, balances and payments followed seasonal trends in the run-up to Christmas. However, while spending rose as expected during November, it was lower year-on-year, signaling continued pressure on household finances.

Average balances resumed an upward trajectory as payment rates dropped to the lowest level since 2021, and overlimit usage increased, meaning risk and collections teams need to be particularly vigilant.

The data showed that spending rose by 2.6% from October to November, reaching an average of £785, but remained 2.4% lower year-on-year. Average active balances reached £1,915, representing a monthly increase of 0.8% and an annual rise of 5%

33.4% of the overall balance was paid in November 2025, 2.8% down on the previous month and 7.4% down on November 2024. The average balances for customers missing payments have increased across all categories, month-on-month and year-on-year

The number of credit card accounts over their limit in November increased by 6.4% month-on-month and 5.9% year-on-year, whilst the percentage of customers using credit cards to take out cash showed the most significant seasonal decline, decreasing by 12.3% from the previous month and 15.2% year-on-year.

FICO said that the combination of the lowest payment rates since 2021 (33.4%) and increasing overlimit usage signals significant financial stress as consumers entered the critical Christmas spending period. With the likelihood of further deterioration in December before some recovery in January, when consumers typically focus on paying off festive spend, risk and collections teams should implement enhanced monitoring for customers showing early warning signs of payment distress.

The continued growth in delinquent balances across all categories indicates that when customers do miss payments, they are doing so with significantly higher debt loads than in previous years. This will make recovery more challenging and require more intensive collection strategies.

Compared to November 2024, there was a mixed picture across accounts with one, two and three missed payments. Improvements were seen in early-stage delinquency, while deterioration was evident in the later stages.

Effective account management decisions must consider a consumer’s current circumstances and ability to afford their current levels of debt, as well as their ability to absorb additional debt – especially if they have recently paid off outstanding balances and their overall behavioural risk has improved. Proactive outreach is a key factor here; it’s the difference between helping a customer stay on track and dealing with a full-blown arrears situation later. It is also at the heart of the Consumer Duty; lenders must ensure any solution offered doesn’t set up the customer to fail.

Source: Credit Connect

Website Launch

Welcom Digital, a trusted provider of loan management systems to the finance sector, has announced the launch of Financier Homeowner, a brand-new module designed to support lenders operating in the residential mortgage sector with an intelligent API first approach providing the tools they need.

Welcom Digital Limited

The Exchange

Station Parade

Harrogate

HG1 1TS

T 0845 456 5859